Disclaimer: This article was originally written by Annabelle Ooi in 2014 and reviewed/edited by the CollegeLAH team in September 2020

FINANCIAL AID PART ONE: JARGONS & CHOOSING UNIVERSITIES

Hello prospective Class of 2019 (and later)! I am Annabelle, a sophomore at Mount Holyoke College. When I applied to American universities, I remember being overwhelmed and frustrated (well… mostly frustrated) by its tedious financial aid application process, a phase I am sure most of you are going through right now. I hope my article does its part in tiding you through the process.

Before we begin, let’s get our terminology straight.

Scholarships (merit-based) versus Financial Aid (need-based)

Merit scholarships are awarded based on merit on the nature of academics/extracurriculars. On many cases merit scholarships alone might not be sufficient to offset the total cost of attendance because they are not tailored to a student’s financial need. However, note that one or more merit scholarships can also be part of a need-based financial aid package.

Need-based financial aid is offered based on your financial need, i.e. the difference between the total cost of attendance of a university and how much your parents/guardians can afford to pay. A typical need-based financial aid package is comprised of one or more of the following: grant, merit scholarship(s), student loan and work-study.

State/public universities generally offer only merit scholarships for international students whereas private research universities and liberal arts colleges usually offer both need-based aid and merit scholarships. UC schools do not offer financial aid for international students but if students are selected for Chancellors’ and Regents’ scholarship after getting an offer, their full financial need will be covered. – include this. Some schools also offer 90% scholarship/financial aid, so you only need to pay just $1000-2000 per year.

Need-aware versus Need-blind

Universities that offer need-based financial aid are either need-aware or need-blind.

Need-blind universities are universities that do not consider your financial need when deciding your admissibility. In other words, applying for financial aid will not “hurt” your chances of being admitted to these universities. Conversely, universities that are need-aware will take into account the fact that you applied for financial aid when considering you for admission.

**In case you still have trouble differentiating the terms I introduced, keep in mind that the word, “need-based”, describes a financial aid policy, whereas the terms, “need-blind” and “need-aware”, are used in relation to admission.

POP QUIZ!

Drawing from what you read earlier, if you are admitted and offered a need-based financial aid package by a university, you now have the financial means to attend this particular university. Is this true? (You have 5 seconds to scroll back and check if you dozed off reading just now.)

*

*

*

*

*

*

The answer is no. (“What?! But you said […]”) Okay, to be fair, that was a trick question. Note that not all universities that offer need-based aid promise to meet 100% demonstrated financial need.

Need-based versus Meets Full Need

Some people might have a hard time differentiating between the concepts of need-based and meeting 100% demonstrated need, so I am going to show some calculations below in regard to this.

Say you, an aspiring scarer, applied to Monsters University and got admitted with a need-based financial aid package.

Total cost of attendance for Monsters University: USD 58000

MINUS

The amount your parents can afford to pay: USD 9500

EQUALS TO

Your financial need: USD 48500

(This is how much financial aid Monsters U should offer you in order for you to attend)

However, Monsters U does not promise to meet full need.

Monsters U adcoms are aware that you need USD 48500-worth of financial aid in order to enroll but unfortunately the university does not have sufficient funding, so you are awarded USD 30000 in financial aid and have until May 1st to decide if you want to enroll.

****** 10-minute water break ******

Choosing universities

The ideal university for a financial aid applicant would, of course, be one that offers need-based aid, is need-blind in terms of admission and promises to meet 100% demonstrated financial aid. Sounds too good to be true? Well, good news for you – they do exist! As of now, there are six need-blind universities in the States that meet full need: Amherst, Harvard, MIT, Princeton and Yale. (Technically, Amherst is a liberal arts college, but for the sake of consistency I will maintain the usage of the term, “university”, in this article.)

“But… as financial aid applicants, we don’t only have five universities to choose from, do we?”

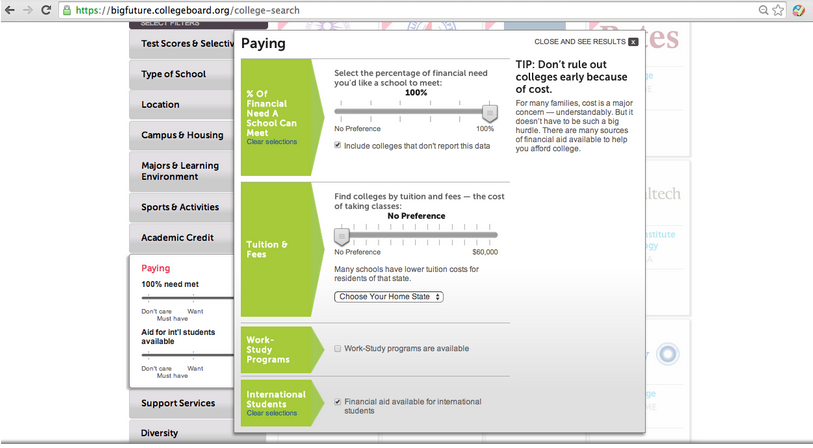

Of course not! There are many universities in the States that, albeit being need-aware, offer need-based aid and promise to meet full need upon admission. When I applied, I had the fortune of stumbling upon a website that had an almost comprehensive list of need-aware, full-need universities. Click on ‘Paying’ on the left-hand side and set the filters to “100% financial need met” and “financial aid available for international students”, voilà – some 69 universities miraculously pop up.

There are, however, two shortcomings about this site:

- There is a very rigid toggle limit for the %-of-financial-need-a-school-can-meet function. The next percentage down from 100 that you can select is 80. Even schools that meet 99.9% need, only 0.1% down from full need, will be ruled out if you set the filter to 100%. I believe that universities that meet more than 98% of financial need should not be ruled out because, speaking from personal experience, there is always the possibility of appealing/negotiating for more aid upon admission.

- Some universities don’t report data on financial aid.

FINANCIAL AID PART TWO: APPLICATION MATERIALS

For international financial aid applicants, you typically submit the CollegeBoard CSS/ Financial Aid PROFILE or the International Student Financial Aid Application (ISFAA). Sometimes the Certificate of Finances (COF) is required along with the ISFAA. In rare cases, some universities, like Bates, Franklin & Marshall, Hamilton and Middlebury, use their own financial aid application forms for international students. In addition to your main financial aid application form, most of the time universities will also ask for certified copies of your parents’ statements of income and tax return forms.

-

CollegeBoard CSS/ Financial Aid PROFILE (Base fee of USD9 + USD16 per university)

This is an online form and the only form that allows you to fill in amounts using Malaysian Ringgit. If you are applying to universities that use a combination of PROFILE and ISFAA and/or COF, I suggest you start with PROFILE and plug in the numbers using the current exchange rate to other forms later.

-

CollegeBoard International Student Financial Aid Application and (sometimes) Certification of Finances (free of charge)

These forms come in .pdf format so you can either complete these forms with Adobe or print them out and fill them in manually. Everything in both forms should be completed in USD.

-

Statement of Income

This would generally be your parents’ monthly pay slips. If they are not in English, translate them into English and have your parents’ employers certify the copies. Companies have these in soft copies – so ask your parents to try to get the soft copies for translation purposes. It does not matter in which currency the amounts are denominated as long as the currency used has been clearly stated. There is no specific requirement as to how many monthly pay slips you should submit, but I submitted three consecutive ones for both parents.

Back when I applied some universities asked for an annual statement of income instead of monthly statements. Neither of my parents’ companies had one of those, so I printed the numbers on my parents’ company letterhead and had my parents’ employers certify them. Below is a template for this in case any of you ever need it.

To Whom It May Concern,

Verification of Annual Income and Taxes Paid in Year 201X

I hereby verify the details of my employee, XXXXXXX as followed:

a) Total Amount of Income Received in Year 201X: RM XXXXX

b) Total Taxes Paid in Year 201X: RM XXXXYours faithfully,

XXXXXXX

-

Tax Return Form

For parents who work in private sectors in Malaysia, this would be the EA form. If you have to translate this form, an English version is readily available in .pdf online. Again, your parents’ employers need to certify these.

FINANCIAL AID PART THREE: MINIMIZING APPLICATION COSTS & OTHER TIPS

The financial cost of applying to American universities can add up, and it doesn’t help that we have to multiply everything by 3.20 or so. Here’s how to not break your (parents’) bank on your way to ‘Murica:

1. Have your college application fee waived (You save:USD 60-80 per school)

Have your school counselor write an application fee waiver request on your behalf, attesting to how the application fee is going to put a strain on your family’s finances. Support with evidence like your annual household income, number of dependants in your family, the total cost of application you have to pay and the current exchange rate. Alternatively, you can write it yourself and have your counselor certify it.

How to submit your college application fee waiver request:

Most colleges want you to mail it physically. However postage can be costly (not as costly as the application fee, but still.) so I asked my counselor to scan and attach the waiver request within her online recommendation letter. For schools that specify they need to receive a fee waiver request before you apply, you can always try sending them a scanned copy of the fee waiver request, explain how posting it will strain your family’s finances, ask if they can accept the scanned copy for now and promise that you will have your counselor send it online along with the rec letter.

How to submit Common App with a fee waiver:

2. Have your test scores sent through counselor (You save: RM100 for IELTS per school and USD11.25 for SATs per school; not sure about TOEFL)

2. Have your test scores sent through counselor (You save: RM100 for IELTS per school and USD11.25 for SATs per school; not sure about TOEFL)

In order to do this, you need to write to individual schools and ask in advance, or schools will deem your application incomplete. You don’t need a formal letter like the fee waiver request; just shoot them an email stating how sending scores via CollegeBoard/ETS/IDP will strain your finances and ask if it’s possible to send them via your counselor instead.

Which score report to submit:

CollegeBoard doesn’t provide you with a physical copy of your SAT test score report unless you request and pay for it. Instead of doing this I downloaded the Online Student Score Report that is available free-of-charge to everyone who has taken the SAT and had my counselor submit the first page of both my SAT I & SAT II reports. There will be a watermark that says “NOT AN OFFICIAL SCORE REPORT” embedded somewhere highly visible on your online report, but fear not – this report will be considered official by most schools once your counselor stamp and certify it.

Where your counselor should attach your test scores:

If you have all your scores ready by the time your counselor submits the Mid-Year Report, have him/her attach them in the Mid-Year Report. Otherwise, wait till all your scores are in and have your counselor submit an Optional Report. I would suggest that you consolidate all test scores and submit them in the same report, i.e. either the Mid-Year Report or the Optional Report. Submitting them separately can be very confusing for the adcoms, and they are already doing you a favor by accepting these score reports via your counselor (this means the extra workload of entering your scores into the system manually), so be considerate!

3. Have your PROFILE fee waived (You save: Base fee of USD9 & USD16 per school)

You do this in two ways:

-

Ask for a PROFILE fee payment code by explaining your financial hardship

For reference, schools that provided me with a code were Amherst, Colorado, Cornell, Duke, Lafayette, Mount Holyoke, NYU and Skidmore. Not all schools offer a fee payment code, though. And if they don’t, go for option b.

-

Ask if they accept the ISFAA and COF in lieu of the PROFILE

Schools that I applied to had varied responses to this. Some agreed to it; some didn’t but agreed to hold off my PROFILE requirement until (if) I receive an admission offer; others sent me their own financial aid application form that they reserve for only students who cannot afford the PROFILE.

4. Have your financial documents (e.g. parents’ statements of income and tax return forms) sent electronically (You save: Whatever postage costs)

Additional Notes:

- The bulk of what I wrote above applies only to those with lower/mid-level household income. If you do not fall under this category and attempt to abuse these fee waivers by misrepresenting your application, know that in life what goes around ultimately comes around.

- When approaching the schools for waivers, be polite but persistent and assertive. You will be surprised at what you can get simply by asking.

- Financial aid applicants should also consider the availability of funding for unpaid summer internships and study abroad programs in a particular university before applying. This might not seem as important at the moment, but – trust me – it will be highly relevant in a year or two.

Annabelle Ooi is a neuroscience major in Mount Holyoke College. She is probably one of the few unartistic left-handers in this world who can’t draw and is tone-deaf. Feel free to email her with questions on financial aid, NeXXt scholar program, liberal arts colleges and life in an all-women’s college.

I see that CSS PROFILE needs a W-2 form. May I know what is that?

LikeLike

Hi, a W-2 form reports wage, income and tax details, and is generally the US equivalent of a Malaysian income tax statement.

LikeLike

isn’t what you said equivalent to tax return form or the EA form? What is the difference between an EA form with W-2 form?

LikeLike